The Nuclear Renaissance 2026: Why AI Just Created the Best Investment Case for Nuclear in 50 Years

- The Financial View

- May 26

- 8 min read

The AI Data Center Paradox

The energy transition was supposed to be simple. Solar gets cheaper. Wind scales. Fossil fuels die. The story made sense until artificial intelligence arrived and rewrote the demand side of the equation in real time.

Here is the paradox the market is slowly pricing in: the same technology companies that spent a decade branding themselves as climate leaders are now signing agreements to restart nuclear reactors that were scheduled for decommissioning. Microsoft, Google, Amazon, and Meta are not doing this because they have abandoned their sustainability commitments. They are doing it because the physics of their data center buildout left them no other choice.

AI data centers currently consume 1-2% of global electricity. The International Energy Agency projects that data center electricity demand will double by 2030. Some independent forecasts put AI-driven consumption at 10% of global electricity within five years. These are not fringe estimates. They come from the same institutions that governments use to set energy policy.

Solar and wind cannot solve this problem. Not because the technology fails, but because of a fundamental physical constraint: they do not generate electricity continuously. A solar panel in Arizona produces power roughly 25% of the hours in a year. A wind turbine in the North Sea operates at around 35-40% capacity. A data center running inference workloads at hyperscale needs power 24 hours a day, every day, with no tolerance for intermittency.

Nuclear operates at a 93% capacity factor. It runs when clouds block the sun. It runs when the wind stops. It runs at 3am on a Tuesday in January. The AI economy accidentally created the most compelling political and economic case for nuclear power in 50 years, and most retail investors have not noticed yet. This research note corrects that.

I. The Electricity Math

The numbers are not subtle. A single ChatGPT query consumes approximately 10 times the electricity of a standard Google search, based on estimates widely cited in academic and industry research. At the scale of billions of queries per day, this compounds into a demand signal that grid operators are only beginning to model.

A single large AI training cluster, the kind used to train frontier models, can consume 50-100 megawatts of continuous power. That is equivalent to the electricity consumption of a city of 40,000 to 80,000 people, sustained around the clock. Google's total data center electricity consumption in 2023 exceeded 24 terawatt-hours, according to the company's own environmental reports. Microsoft consumed 18 terawatt-hours the same year. Combined, those two companies alone consume more electricity than many European nations.

The IEA's Electricity 2024 report projects that global data center electricity demand will reach 945 terawatt-hours by 2026, up from 415 terawatt-hours in 2022. By 2030, the agency's central scenario sees data center demand approaching 1,000 terawatt-hours annually in the United States alone.

The capacity factor problem is the crux of why renewables cannot fill this gap alone. Capacity factor measures the ratio of actual electricity output to maximum possible output over a period. Nuclear runs at 93%. Natural gas combined cycle operates around 57%. Coal averages 49%. Wind, depending on location, lands between 30-40%. Utility-scale solar in the best markets reaches 25-30%.

Grid-scale battery storage is the proposed solution to renewable intermittency, but the economics remain prohibitive. The cost to store enough energy to back a single large data center for 24 hours of renewable-only operation runs into hundreds of millions of dollars in battery infrastructure alone, before accounting for land, interconnection, and replacement cycles. Transmission infrastructure is a separate constraint: data centers are being built in locations where grid capacity does not exist, and building new high-voltage lines takes 10-15 years in the United States.

Nuclear does not need storage. It does not need favorable weather. And unlike gas peakers, it does not produce carbon. For the AI economy, this makes it the only existing technology that solves all three problems simultaneously.

II. Why Now Is Different

Three structural shifts between 2024 and 2026 changed the nuclear investment calculus in ways that prior bull cycles failed to deliver.

Corporate Power Purchase Agreements

The most important catalyst is not government policy. It is corporate procurement. Microsoft signed a 20-year power purchase agreement in September 2023 with Constellation Energy to restart Unit 1 at Three Mile Island, the same plant associated with the 1979 accident that effectively ended the first nuclear era. The restart is scheduled for 2028. Amazon Web Services signed PPAs with Dominion Energy and Talen Energy for nuclear-adjacent power. Google signed an agreement with Kairos Power for small modular reactor output, the first such agreement between a major technology company and an SMR developer.

These are not symbolic commitments. They are binding commercial agreements worth billions of dollars, structured over 10-20 year terms, providing exactly the long-duration contracted revenue that utilities need to justify nuclear investment. The corporate PPA market has done in 24 months what two decades of nuclear advocacy could not: provide bankable demand.

Small Modular Reactor Technology

The second catalyst is technological. Traditional nuclear plants require enormous capital and a decade-plus construction timeline. Small Modular Reactors, defined as reactors below 300 megawatts, are designed to be factory-built, modular, and deployable faster than conventional plants.

NuScale Power became the first SMR design to receive Nuclear Regulatory Commission design approval in 2022, a process that took years and represented a landmark in US nuclear licensing. Oklo Inc, backed by Sam Altman of OpenAI, received its combined license application acceptance from the NRC in late 2023 and signed its first commercial customer agreements in 2024. TerraPower, funded by Bill Gates, has broken ground on its Natrium reactor in Wyoming.

Political Consensus

The third catalyst is political, and it is the most durable. For the first time since the 1970s, nuclear energy commands genuine bipartisan support in the United States. The Inflation Reduction Act of 2022 extended and expanded the Production Tax Credit for existing nuclear plants through 2032, worth approximately $15 per megawatt-hour of nuclear output. The ADVANCE Act, passed in 2024, directs the NRC to streamline licensing, reduce fees for advanced reactor applicants, and create incentives for deploying reactors in communities that host decommissioned plants.

The political risk that defined nuclear investing for 40 years has materially diminished.

III. The Investment Universe

Five instruments give investors differentiated exposure to this thesis across the risk spectrum.

Constellation Energy (CEG) — Our Current Holding

Constellation is the safest, most direct expression of the nuclear thesis. The company operates 21 reactors across the United States, making it the largest nuclear fleet owner in the country. The Three Mile Island PPA with Microsoft is a landmark transaction: a 20-year agreement that provides contractual revenue certainty of a type nuclear plants have historically lacked.

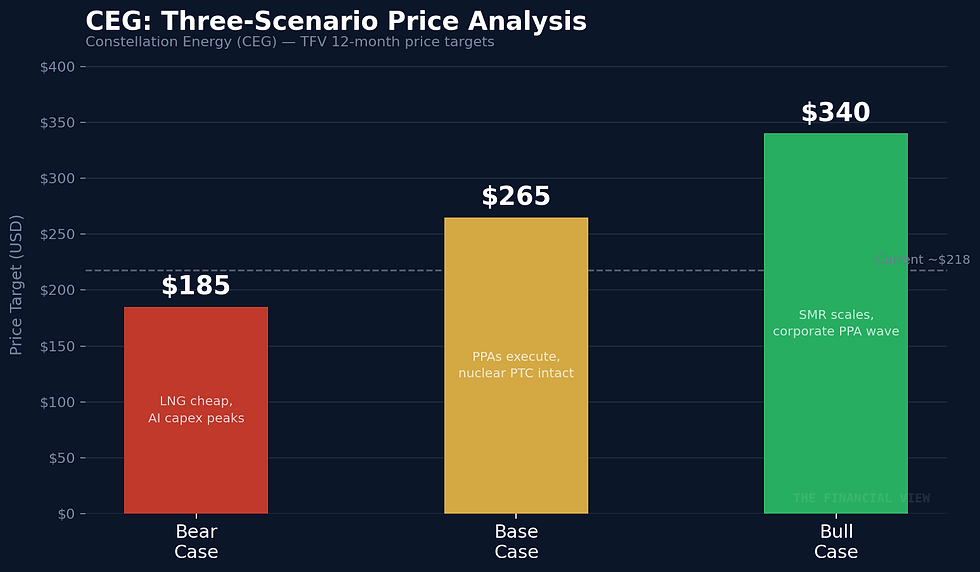

CEG has authorized a $5 billion share buyback. The balance sheet is investment grade. The company is profitable today, not contingent on SMR technology that has never been built at commercial scale. For a thesis this structural, we want the asset base that is already operating and already contracted. CEG is that asset. Our view: Strong Buy. Price target $265 base case, $185 bear, $340 bull.

Cameco Corporation (CCO) — Uranium Commodity Play

Cameco is the world's largest publicly listed uranium producer, headquartered in Canada, with operations in Saskatchewan and Kazakhstan. Uranium spot prices have risen approximately 80% since 2022, from roughly $40 per pound to above $70 per pound for U3O8, driven by supply constraints, reactor restarts in Europe, and new demand from both conventional plants and SMR commitments.

Cameco provides direct commodity exposure to the uranium fuel cycle. The Cigar Lake and McArthur River operations are among the highest-grade uranium deposits on the planet. Long-term contract pricing remains below spot, which means as existing contracts roll off, realized pricing should improve further. Our view: Buy.

Global X Uranium ETF (URA) — Broad Sector Exposure

For investors who want diversified exposure across the uranium mining ecosystem without single-name concentration risk, URA provides access to Cameco, Uranium Energy Corp, NexGen Energy, and a range of smaller producers. The ETF does not provide leverage to nuclear utilities, only to the fuel supply chain. It is the appropriate instrument for investors who believe uranium prices will continue rising but want to avoid individual operator risk. Our view: Hold for diversification.

Oklo Inc (OKLO) — SMR Pure Play, High Risk/Reward

Oklo is a pre-revenue small modular reactor company. Sam Altman, chairman of OpenAI, serves as chairman of Oklo's board. The company's Aurora reactor design targets commercial deployment in the late 2020s. Oklo has signed Letters of Intent and customer agreements for its first commercial plants, but no revenue exists and the technology has not been built at scale.

This is a 5-year option, not a 12-month trade. The upside if SMR commercialization succeeds is generational. The downside if the technology, licensing, or financing fails is substantial. Appropriate position sizing is small. Our view: Speculative Buy. Size accordingly.

Centrus Energy (LEU) — Critical Infrastructure Play

Centrus is the only US company licensed by the NRC to produce High-Assay Low-Enriched Uranium (HALEU), the fuel required by most advanced reactor designs including Oklo and TerraPower. This is a structural monopoly position in a supply chain the United States government has explicitly identified as a national security priority. The DOE signed cost-sharing agreements with Centrus specifically to develop domestic HALEU production capacity.

HALEU supply is currently insufficient to support the commercial SMR pipeline. As SMR deployments accelerate, Centrus becomes a critical bottleneck. Our view: Buy.

IV. The Tail Risks

No thesis is complete without an honest accounting of what breaks it.

Permitting delays remain the most persistent structural risk in US nuclear development. The NRC licensing process, despite legislative reform under the ADVANCE Act, still operates on timelines measured in years. The cost of capital for a delayed nuclear project compounds adversely.

Construction cost overruns are documented. Vogtle Units 3 and 4 in Georgia, the only new nuclear units completed in the United States in decades, came in approximately $17 billion over budget and years behind schedule. The lesson is not that nuclear cannot be built, but that first-of-a-kind construction carries substantial execution risk.

SMR execution risk is real and underappreciated in the equity prices of pre-revenue companies. No SMR has been built at commercial scale in the Western world. Engineering challenges at scale may produce timeline and cost outcomes inconsistent with current projections.

Natural gas competition is the most underrated risk. If LNG prices remain depressed, gas-fired generation provides baseload competition to nuclear at far lower capital costs. A sustained period of cheap gas weakens the economic case for new nuclear investment.

Public opposition remains latent. A single high-profile nuclear incident anywhere in the world reprices the sector within hours.

V. Our Take

CEG is the trade. It is profitable, it is contracted, it is in our book. The Three Mile Island restart with Microsoft as the offtaker is the kind of landmark commercial transaction that defines a new era in an industry. The $5 billion buyback provides a floor under the equity.

For investors with higher risk tolerance, CCO provides clean uranium commodity exposure with a balance sheet strong enough to withstand a commodity pullback. The long-term contract roll-off dynamic means the earnings upside is not fully priced.

Oklo is a conviction position for investors with a five-year horizon and appropriate position sizing. Do not chase the name on the back of Sam Altman headlines alone. The technology must be built, licensed, and connected to the grid before revenue materializes. Size this as a venture allocation, not a core holding.

The broader point: the nuclear investment thesis has moved from a political argument to a commercial reality. Corporate PPAs, bipartisan legislation, and AI power demand have done the work. The market is pricing this in, but not completely. There is still time.

VI. What Would Change Our Mind

Three developments would cause us to materially reduce nuclear exposure.

First, sustained LNG prices below $3 per MMBtu for 18 or more months would make gas-fired generation so cheap that corporate buyers would redirect their PPAs away from nuclear. Data center operators are agnostic to the source of baseload power; they want reliability at competitive cost.

Second, a material deceleration in AI capital expenditure, particularly a reduction in data center buildout commitments from hyperscalers, would remove the demand catalyst driving the current bull case. Any credible signal that AI capex has peaked warrants a reassessment of the power demand trajectory.

Third, a major SMR project failing a safety review at the NRC would reset the SMR timeline by years and reprice the pre-revenue names significantly.

We are watching all three. None of them are our base case.

Disclaimer

This research is for educational purposes. Not investment advice. The Financial View operates a virtual $100,000 portfolio for educational tracking. We hold a long position in CEG.

Comments