Startup Nation: How a Country of 9 Million Built the World's Most Resilient Tech Economy

- The Financial View

- May 18

- 17 min read

THE FINANCIAL VIEW | GLOBAL MACRO DEEP DIVE | MAY 2026

I want to tell you about a country that has been bombed, sanctioned, diplomatically isolated, and written off more times than I can count — and has responded each time by compounding faster than almost any economy on earth.

In March 2026, Google quietly closed the largest acquisition in its 28-year history: $32 billion, all cash, for a four-year-old Israeli cybersecurity startup called Wiz. The previous year, Palo Alto Networks announced a $25 billion bid for CyberArk. ServiceNow paid $7.75 billion for Armis. In 2025 alone, Israeli tech exits totalled somewhere between $58 billion and $89 billion — the second-largest year in the country's history, behind only the 2021 IPO boom.

All of this happened while Israel was fighting a multi-front war — against Hamas in Gaza, Hezbollah in Lebanon, the Houthis across the Red Sea, and Iran directly. In June 2025, missiles hit residential blocks in Tel Aviv, Ramat Gan, and Haifa. Ben Gurion Airport was struck in May 2025. In March 2026, Hezbollah reignited fighting on the northern border.

The TA-35 Index returned +51.6% in 2025. The shekel, by May 2026, was trading at its strongest level since 1993. FX reserves hit a record $235.7 billion. And two of the three major rating agencies upgraded their outlooks to stable.

This is not a coincidence. This is a system — one built deliberately over 40 years through a specific combination of policy decisions, military architecture, mass immigration, and institutional design. And understanding how it works is, I think, one of the most important macro stories of the next decade.

PART ONE: THE FOUNDATION — HOW HYPERINFLATION BECAME A TECH ECOSYSTEM

To understand the Startup Nation, you have to go back to 1984 — when Israel was facing an economic catastrophe that would have ended most countries' growth stories before they began.

Inflation was running at 445% annually. Monthly price increases were exceeding 15%. The fiscal deficit had reached 16% of GDP. Foreign debt was exploding. Economists were projecting 1,000%-plus hyperinflation by year-end if nothing changed. The Israeli economy, at that moment, looked more like Argentina than a future technology powerhouse.

What happened on July 1, 1985 is one of the most underappreciated economic interventions of the 20th century. Chief Economist Michael Bruno, working with American advisor Stanley Fischer (who would later run the Federal Reserve as Vice Chair) and Finance Minister Yitzhak Moda'i, implemented what became known as the Economic Stabilization Plan. It was a heterodox package that combined a 20% shekel devaluation with an immediate freeze on wages, prices, and the exchange rate — simultaneously. The government cut the deficit by 7.5% of GDP in a single year. A $1.5 billion emergency backstop from the United States was secured.

The results were almost implausible: inflation collapsed from 445% in 1984 to 185% in 1985, then 20% in 1986, then 16% in 1987. GDP growth averaged 5% per year through 1986 and 1987. Israel had stabilised itself.

This matters because the 1985 stabilisation created the preconditions for everything that followed. Without price stability and a credible currency, there is no venture capital. Without venture capital, there is no Startup Nation. The entire edifice rests on a crisis that was solved by a few economists working against a very short deadline.

It was also in 1984 that the Israeli government passed the R&D Law, establishing what became the Office of the Chief Scientist — the institutional ancestor of today's Israel Innovation Authority. This body would become the chassis on which the entire tech ecosystem was built.

The Yozma Program: How $100 Million Became a $3.3 Billion Industry in Seven Years

In 1993, Chief Scientist Yigal Erlich launched the Yozma Program with $100 million in government capital. The design was remarkably clever. $80 million seeded ten private venture capital funds. Each fund was structured as a three-way partnership: an Israeli nascent VC firm, a foreign VC partner (firms like Advent International, Daimler-Benz's VC arm, and Walden International), and an Israeli financial institution. The government took a 40% equity stake. But private investors were given a call option to buy out that government stake at the original cost plus only 5-7% annual interest — an extraordinarily favourable asymmetry that made participation almost irrational not to pursue.

Nine of the ten fund GPs exercised that buy-out option. The result: Israeli VC investment expanded from $5 million in 1990 to $3.3 billion by 2000 — a 660-fold increase in a decade. The number of foreign investment banks operating in Israel went from 1 to 26. The government's Yozma stake was fully privatised by 1998.

The genius of Yozma was not just capital — it was the foreign VC partner requirement. Those partners brought Silicon Valley networks, deal expertise, and international credibility that Israeli founders had never had access to. They created the connective tissue between Tel Aviv and Sand Hill Road.

The Soviet Aliyah: A Talent Shock Unlike Anything in Economic History

Between 1989 and 2000, approximately one million Soviet Jews emigrated to Israel. To understand the scale of this: Israel's pre-wave population was 4.5 million. This was a 20% population shock absorbed in roughly a decade.

But it was the composition that was historically unprecedented. Roughly 60% of the 1989-1990 arrivals had post-secondary education. Two-thirds held scientific, academic, or technical occupations. Between 1990 and 1993 alone, 57,000 engineers and 12,000 physicians arrived. Before the wave, Israel had approximately 30,000 engineers and 15,000 doctors. The engineer workforce nearly tripled in three years.

Israeli economist Shlomo Maoz captured it plainly: "The Russians saved Israel, big time." By 2000, Israel had roughly 140 engineers and scientists per 10,000 workers — among the highest concentration globally, and the raw talent base that would staff the VC-funded startup ecosystem that Yozma had just created.

Unit 8200: The World's Most Productive Founder Factory

Every country has a military. Very few militaries function as an elite technology incubator that graduates founders into a waiting venture capital ecosystem at age 21.

Unit 8200 is the signals intelligence branch of the Israeli Defense Forces, subordinate to Military Intelligence (Aman). RUSI, the British defense think tank, has described it as "probably the foremost technical intelligence agency in the world, on a par with the NSA in everything except scale." It has approximately 5,000 active-duty soldiers at any given time, conscripted at age 18-21 and selected through nationwide screening that identifies the top mathematical and technical talent in the country.

The alumni list reads like a Forbes list of cybersecurity. Gil Shwed founded Check Point Software in 1993 — the first commercial firewall, now a $12 billion company. Nir Zuk, who built the core engine at Check Point, left to found Palo Alto Networks in 2005 — now worth nearly $200 billion. Udi Mokady founded CyberArk in 1999. Four alumni who met on the bus to IDF induction on July 16, 2001 — Assaf Rappaport, Ami Luttwak, Roy Reznik, and Yinon Costica — built Adallom (sold to Microsoft for $320 million in 2015) and then, in January 2020, founded Wiz. Four years later, Google paid $32 billion for it.

A 2018 academic study found that 80% of Israeli cybersecurity founders had IDF intelligence experience. Five publicly traded 8200-alumni cybersecurity companies were collectively valued at approximately $160 billion on US exchanges in 2024. The unit has also produced Waze (sold to Google for $1.1 billion), Viber, and Wix — the website platform that hosts The Financial View.

PART TWO: THE NUMBERS — WHAT THE DATA ACTUALLY SAYS

Let me put some numbers around what is happening in Israel's economy right now, because the data is extraordinary — and largely underreported in Western financial media.

Israel's tech sector generates approximately NIS 317 billion annually — roughly $83 billion, or 17.3% of GDP. If you use a cash-flow basis rather than output, Startup Nation Central estimates it at closer to 20%. This sector employs 403,000 people, which is 11.5% of the workforce. Those workers earn an average monthly wage of NIS 31,858 — compared to a national average of NIS 13,514. The tech sector pays 2.36 times the national average wage, and it contributes approximately 36% of all wage-related income tax revenue despite employing only 11.5% of workers.

In 2024, tech exports reached $78 billion — 56.4% of all Israeli exports. In the first half of 2025, that share hit 57.2%, an all-time record. And here is the structural point that most analysts miss: 72% of those tech exports are services and software. They cannot be physically bombed. A missile cannot destroy a SaaS contract. This is why the tech sector grew 2.2% in the first three quarters of 2024 even as the broader Israeli economy contracted 1.5% — the supply side of the most important part of the economy has structurally decoupled from kinetic conflict.

The Shekel Story: From 11-Year Lows to Strongest Since 1993

In the two weeks following the Hamas attack on October 7, 2023, the Israeli shekel fell to 4.0855 per dollar — an 11-year low. Markets were pricing in a protracted, catastrophic conflict. The Bank of Israel responded on October 9 by announcing a $30 billion FX intervention program — the first such program in the country's history — plus an additional $15 billion in swap liquidity. The announcement alone was enough to halt the rout. The Bank ultimately deployed only $8.5 billion of that $30 billion, roughly 28% of its declared firepower. The threat was sufficient.

By May 11, 2026, the shekel was trading at 2.89 per dollar — its strongest level since October 1993. The currency had appreciated 18.2% year-on-year against the dollar. On May 6, it had briefly broken below 3.00 for the first time since 1995. An investor holding Tel Aviv equities in dollar terms earned +72% in 2025 versus +52% in local currency, because the shekel's re-rating was doing the extra work.

The Bank of Israel's foreign exchange reserves sat at a record $235.7 billion in April 2026 — 38.4% of GDP — up from $198 billion before the October 7 attack. This is not a country running out of firepower. This is a country that has been accumulating ammunition throughout a war.

The TA-35: Best-Performing Major Index on Earth in 2025

The Tel Aviv Stock Exchange TA-35 index returned +51.6% in 2025, compared to +21.6% for the S&P 500 and +17.7% for the Nasdaq-100. The FTSE 100, which had a strong year by European standards, returned +25%. Over the two-year period since October 2023, the TA-35 has returned approximately +100%.

The sector breakdown for 2025 tells you exactly what drove it. Insurance stocks returned +152%. Financial services returned +134%. Banks returned +61-68%. Energy infrastructure returned +71-77%. The defense-adjacent names have been extraordinary: Aryt Industries, which makes defense fuzes, is up approximately 2,212% since October 2023.

Foreign institutional holdings of Israeli equities hit a record $19.2 billion by September 2025 — more than double their pre-war levels — with 80% coming from North American institutions. The market is not betting against the geopolitical risk. It is betting through it.

Sovereign Credit: The Market Has Already Decided

In September 2024, Moody's cut Israel's credit rating by two notches to Baa1 — the largest single downgrade in the country's history. It was, by any measure, alarming. But by January 2026, Moody's had upgraded the outlook to stable. S&P had done the same in November 2025. The five-year sovereign CDS spread, which had peaked above 150 basis points during the worst of the Hezbollah escalation in mid-2024, was trading near 60-80 basis points by May 2026 — back to pre-war levels.

In January 2026, Israel issued $6 billion in sovereign dollar bonds across three tranches — 5-year, 10-year, and 30-year. The weighted spread over US Treasuries was 102 basis points. That is 34% tighter than the 154-basis-point weighted spread Israel paid in its 2024 issuance. The order book hit $36 billion — six times oversubscribed — with more than 300 investors from 30 countries. The bond market is not a sentiment indicator. It is the most coldly rational pricing mechanism in finance. When 300 institutions from 30 countries six-times oversubscribe an Israeli sovereign bond at tighter spreads than the previous year, that is a verdict.

PART THREE: THE COMPOUNDERS — THE COMPANIES BUILDING ISRAEL'S ECONOMIC MOAT

Cybersecurity: The Industry Israel Owns

The global information security market was $213 billion in 2025 and is forecast to reach $244 billion in 2026 and $322 billion by 2029. Israel captures more than 20% of global deep-tech cyber investment despite having an economy that represents a tiny fraction of global GDP. In 2025, Israeli cyber startups raised $4.4 billion — approximately one-fifth of everything invested in cybersecurity worldwide.

The Wiz story deserves careful attention because it illustrates something important about how Israeli tech has evolved. Assaf Rappaport and his three co-founders launched Wiz in January 2020. Within 18 months, they had reached $100 million in annual recurring revenue — the fastest any software company in history had reached that milestone. By February 2024, ARR was $350 million. By July 2024, $500 million. By March 2025, it crossed $1 billion. In July 2024, Google offered $23 billion. Rappaport rejected it. In March 2025, Google offered $32 billion — 39% more. Wiz accepted. The deal closed March 11, 2026.

Palo Alto Networks, founded by 8200 alumnus Nir Zuk, generated $8 billion in revenue in fiscal year 2025 and is guiding to $11.3 billion in fiscal year 2026 — 22% growth. Its Next-Generation Security ARR hit $6.33 billion in the most recent quarter, up 33% year-on-year. The company's acquisition of CyberArk for $25 billion — which combines Palo Alto's network and cloud security with CyberArk's identity and privileged access management — creates the first platform in the industry that genuinely covers network, cloud, SecOps, and identity security under one architecture.

AI Infrastructure: The Invisible Layer Israel Runs

Here is a fact that most people in finance still have not fully absorbed: the connective tissue of global AI infrastructure is Israeli-designed.

In 2020, Nvidia acquired Mellanox Technologies — a networking company founded in 1999 in Yokneam, Israel — for $6.9 billion. That acquisition has since generated more revenue per quarter than the original purchase price. In Nvidia's most recent quarter, the networking segment produced $7.25 billion — up 46% quarter-on-quarter and approximately doubling year-on-year. The annual run rate is somewhere between $25 and $30 billion from a single $6.9 billion deal.

Nvidia now employs more than 5,000 people in Israel — more than double its pre-acquisition headcount there — and is planning what will become the country's largest private-sector tech campus. Jensen Huang has described Spectrum-X, which was developed substantially in Israel, as "a home run" and "quite a sizable business that is only about 1.5 years old." The Rubin platform unveiled at CES 2026 includes five chips with significant Israeli development: the Vera CPU, NVLink 6 Switch, ConnectX-9, BlueField-4, and Spectrum-6.

Apple's second-largest R&D center outside the United States is in Herzliya and Haifa, led by Johny Srouji — a Haifa-born senior vice president who is the head of Apple's chip design. The Israeli teams have been central to the M1 and M2 chips, the Vision Pro R1 chip, and they built Apple's first cellular modem, the C1, as well as Apple's first AI server chip. Google, Amazon, Microsoft, Meta, AMD, and Cisco all maintain major R&D operations in Israel. There are more than 570 multinational R&D centers in the country.

Defense: The War-Driven Compounder

If you have been following European rearmament news, you have been reading about Israeli defense companies without necessarily knowing it.

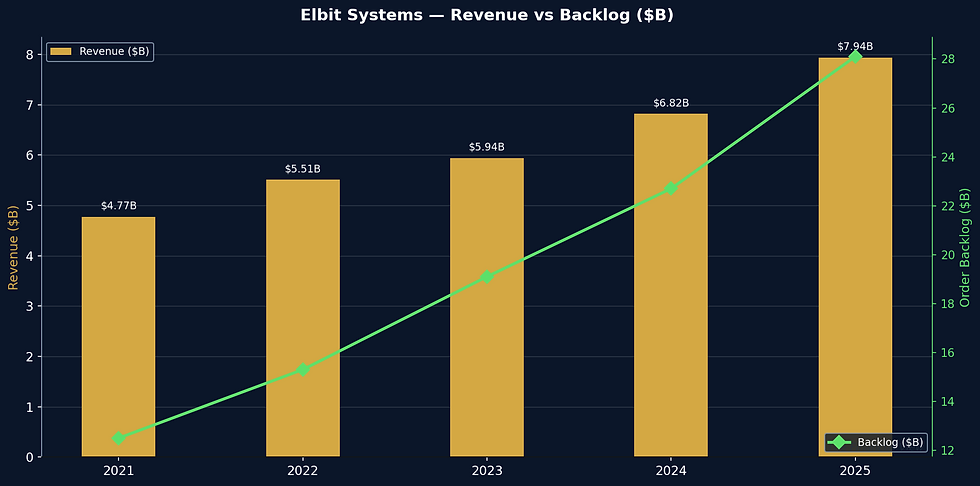

Elbit Systems generated $7.94 billion in revenue in 2025 — up 16.3% — with a backlog of $28.1 billion, which represents approximately 3.5 times annual revenue. That backlog grew by $5.5 billion, or 24%, in a single year. European revenue has grown 106% over the past three years, from $885 million in 2021 to $1.82 billion in 2024, driven by demand post-Ukraine. In March 2026, Bloomberg reported Germany negotiating a contract worth up to €6 billion for rockets with Elbit — alongside Rheinmetall.

Israel Aerospace Industries — state-owned — generated $7.38 billion in revenue in 2025, up 21%, with a backlog of $28.96 billion and net income up 45% to $712 million. Its Arrow 3 missile defense system sale to Germany — initially a $3.5 billion contract in 2023, expanded to an additional $3.1 billion in January 2026 — represents the largest defense export deal in Israeli history at a combined $6.5 billion. The first battery was delivered to Holzdorf Air Force Base in December 2025.

Israeli defense exports reached a record $14.8 billion in 2024 — double the level of five years ago. Europe, which accounted for 36% of Israeli defense exports before the Ukraine war, now represents 54%. The product mix tells you everything about where the threat environment is: missiles, rockets, and air defense systems represent 48% of export value. Satellite technology went from 2% to 8%.

The R&D Advantage: No. 1 in the World

Israel spent 6.35% of GDP on civilian R&D in 2023 — the highest ratio of any country in the world, according to OECD data. South Korea is second at 5.0%. The United States is at 3.45%. The OECD average is 2.7%. The EU average is 2.1%. Israel invests in research at roughly 2.4 times the rate of the average advanced economy. This is not a recent phenomenon — it is a structural characteristic that has compounded for decades.

Per $100 billion of GDP, Israel produces 11 unicorns — more than any country in the world, ahead of Singapore at 10 and the United States at 6.2. There are 42 active Israeli-headquartered unicorns as of May 2026, with Tel Aviv ranking fifth globally as a startup hub. This is a country with a population roughly equal to Switzerland, Sweden, or Hong Kong.

PART FOUR: THE PATTERN — WARS AND RECOVERIES

One of the most reliable patterns in Israeli economic history is what happens immediately after major conflicts. The 2006 Lebanon War lasted 34 days and cost approximately $2.4 billion — 1.3% of GDP at the time. The GDP hit during the conflict was approximately 0.35-0.5%. The full-year 2006 growth rate was 5.7%, and 2007 came in at 6.9%. Recovery was essentially complete within a year.

Operation Protective Edge in 2014 lasted 50 days. Full-year GDP growth was 2.2% despite the disruption, with a Q4 rebound. Operation Guardian of the Walls in 2021 lasted 11 days. The private sector cost was roughly $54 million per day. Full-year 2021 GDP growth was 8.6%.

The current conflict — the Iron Swords War, which began October 7, 2023 — has been categorically larger in scale and duration than any previous episode. The Q4 2023 GDP contraction was -21.7% on an annualised basis. But the Q1 2024 rebound was +14.1 to +15.6%. The 12-Day War with Iran in June 2025 caused a Q2 2025 contraction of -4.6%, followed by a Q3 2025 rebound of +12.7% — a record single-quarter bounce. The Bank of Israel projects 2026 growth at 3.8% (raised from an earlier 5.2% estimate due to the Roaring Lion operation in February-April 2026). The IMF's estimate is 4.8%.

The pattern is consistent and increasingly pronounced: each conflict produces a sharp but short contraction, followed by a recovery that frequently exceeds the pre-conflict trend. And each cycle, the tech sector decouples a bit more strongly from the rest of the economy.

PART FIVE: THE HONEST RISKS — WHERE THE THESIS CAN BREAK

I am not going to write about Israel's economic resilience without being equally honest about the risks, because some of them are serious and at least one is genuinely alarming.

Brain Drain: The Long-Tail Erosion

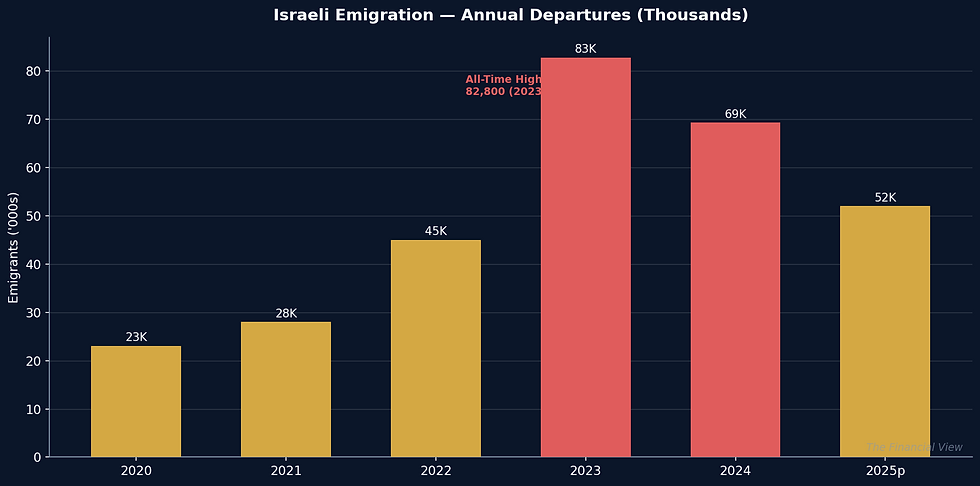

In 2023, 82,800 Israelis emigrated — an all-time high. A study by Tel Aviv University economists, published in December 2024, found that 90,000 people left in the 21 months from January 2023 through September 2024, including 633 STEM PhDs and approximately 3,000 engineers. To understand the scale: in all of 2022, 285 PhDs and 1,039 engineers had emigrated.

Data from the Shoresh Institute finds that 25.4% of Israeli math PhDs and 21.7% of Israeli computer science PhDs are living abroad. In 2025, approximately 50% of new Israeli startups incorporated in the United States rather than in Israel — compared to 75-80% incorporating domestically in 2018-2022. Bessemer Venture Partners partner Adam Fisher, who runs the firm's Israel operations, stated in 2025 that "more than 80%" of new startups are choosing to register in the US.

This matters for tax revenue as much as it matters for talent. Wiz, incorporated in Delaware, generated a projected 10 billion shekels ($3.2 billion) in Israeli tax revenue from its $32 billion sale — primarily from founders' personal taxation. CyberArk, incorporated in Israel, will generate substantially more for the Israeli treasury from its $25 billion sale. Each Delaware incorporation represents a permanent reduction in Israel's future tax base, even when the founders remain physically in Tel Aviv.

Military Risk: Iran Is Damaged, Not Eliminated

The 12-Day War in June 2025 — when Israel struck 27 Iranian provinces and the United States joined on June 21 to hit Natanz, Isfahan, and Fordow — significantly degraded Iran's ballistic missile capacity. Before the war, Iran had an estimated 2,500-3,000 ballistic missiles and approximately 480 mobile launchers. Post-war estimates from the Alma Center (February 2026) suggest approximately 1,000-1,200 serviceable missiles remain, with mobile launchers down to roughly 100 from 480 — an 80% reduction in launch capacity.

But the 12-Day War also exposed the limits of missile defense. Israel burned through Arrow interceptors faster than anticipated. The United States fired approximately 150 THAAD interceptors and around 80 SM-3 missiles — described as "a quarter of US stockpile and several years' worth of production." New THAAD deliveries are not expected until April 2027. And during the fighting, residential areas in central Tel Aviv, Ramat Gan, and Haifa were struck. 240 residential buildings were damaged, more than 2,000 apartments hit, 9,000 people displaced.

The 2026 Lebanon War — reignited March 2, 2026 after Hezbollah launched the first projectiles since the November 2024 ceasefire — remains ongoing as of this writing. More than 2,800 people have died in Lebanon, and more than a million have been displaced. This is not a contained situation.

Fiscal: The Deficit Is Real

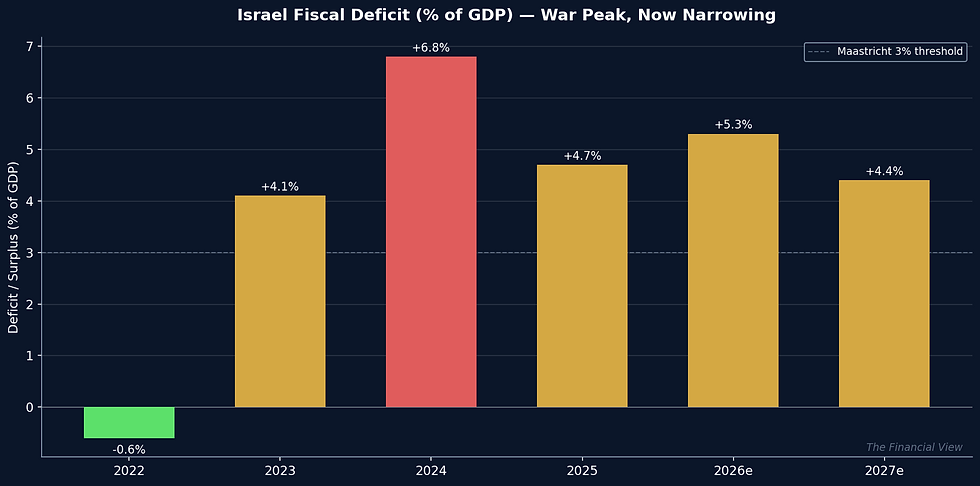

The cumulative cost of the Iron Swords War is estimated by the Bank of Israel at NIS 250-255 billion — roughly 13% of GDP. Defense spending in 2025 was approximately NIS 163 billion, or roughly 8% of GDP. The fiscal deficit peaked at 6.8% of GDP in 2024 and was projected at 5.3% for 2026 as of the Bank of Israel's March forecast. Debt-to-GDP has risen from 60.5% in 2022 to approximately 70% in 2025.

The positive offset is that 2025 state revenue hit NIS 551.9 billion — up 13.8% year-on-year — driven partly by the Wiz/Google exit tax windfall and partly by the VAT increase from January 2025. S&P projects debt-to-GDP back to 67% by 2028. The trajectory is narrowing, but it requires sustained growth and fiscal discipline during an active war.

VC Formation: The Structural Gap

Here is the most important nuance in the bullish thesis: capital deployed into Israeli startups was strong in 2025 ($15.6 billion, above pre-war levels), but Israeli VC fundraising — the formation of new local funds — has collapsed. In the first half of 2025, only 12 funds raised capital, totalling $260 million. In 2022, 62 funds raised $5.9 billion. The dry powder available for new seed and early-stage investments fell to $208 million — 2017 levels.

What this means is that foreign capital is flowing in at the growth and late stages — the Googles and Palo Alto Networks of the world buying proven companies — while the domestic engine that creates the next generation of startups is running on empty. This is a structural risk that plays out over a 5-10 year horizon rather than a 12-month horizon, but it is the most important long-term data point I am tracking.

PART SIX: THE MACRO CATALYST — WHAT COULD CHANGE EVERYTHING

The base case for Israel — gradual de-escalation, risk premium compression, GDP growth of 4-5% in 2026 and 2027, TA-35 returning +15-25% — is already a compelling investment thesis given current valuations.

The bull case is Saudi normalization. I assign roughly a 15-20% probability over the next 24 months, and INSS and the Middle East Institute both suggest it has been slipping away in the near term. Crown Prince Mohammed bin Salman has made a Palestinian state with East Jerusalem as its capital a precondition. But if it happens, RAND estimates the resulting regional integration would unlock more than $1 trillion in regional GDP and 4 million jobs. Tel Aviv equity multiples would re-rate toward Gulf peers. The shekel would hit levels not seen in modern memory. Every Israeli bank, real estate firm, and tech company with Middle East exposure would trade materially higher.

The bear case — re-escalation, a second full-scale Iran exchange, a coalition government collapse triggering elections, or a prolonged Lebanon war that bleeds more engineers and founders abroad — would likely produce a TA-35 drawdown of 15-25%, a shekel reverting to the 3.80-4.20 range, and a sovereign credit downgrade back to negative outlook. Defense names would still outperform in this scenario. Everything else would be painful.

THE BOTTOM LINE

Israel is a country that has done something no economic textbook would have predicted: it has built a globally dominant, structurally irreplaceable technology ecosystem in a geography under constant existential military pressure. The mechanism is not magic — it is 40 years of compounding decisions. The 1985 stabilisation created the macro precondition. Yozma in 1993 created the VC infrastructure. The Soviet aliyah in 1989-2000 tripled the engineer base. Unit 8200 has been running a continuous talent factory since 1952. The result is a country where 11.5% of the workforce generates 36% of income tax revenue, 57% of all exports, and an outsized share of the world's most critical AI and cybersecurity infrastructure.

The risks are real. The brain drain is accelerating. The domestic VC formation has cratered. The Lebanon war has resumed. The fiscal deficit is elevated. Saudi normalization is not imminent. These are not dismissible.

But the market is telling you something with $36 billion in demand for a $6 billion sovereign bond, a shekel at its strongest since 1993, a TA-35 that has doubled since October 7, and $32 billion from Google for a four-year-old startup. What it is telling you is that global capital has looked at the conflict, the brain drain, the fiscal deficit, and the geopolitical uncertainty — and decided that the IP is irreplaceable, the compounders compound regardless, and the risk premium does not adequately compensate for missing the upside.

I think global capital is right.

This research is for educational purposes. Not investment advice. The Financial View operates a virtual $100,000 portfolio for educational tracking.