Advanced Micro Devices (AMD): The Second Act — Full Institutional Equity Research Report

- The Financial View

- May 21

- 10 min read

Advanced Micro Devices (AMD): The Second Act

Full Institutional Equity Research Report | The Financial View | May 2026

Investment Rating: STRONG BUY | Price Target (12-Month Base Case): $480 | Current Price (May 20, 2026): ~$416 | Upside: ~15% | Rating: ⭐⭐⭐⭐½

"AMD is no longer the challenger. It is the alternative — and in the $500B AI infrastructure buildout, having a credible alternative is worth hundreds of billions of dollars in revenue over the next five years."

EXECUTIVE SUMMARY

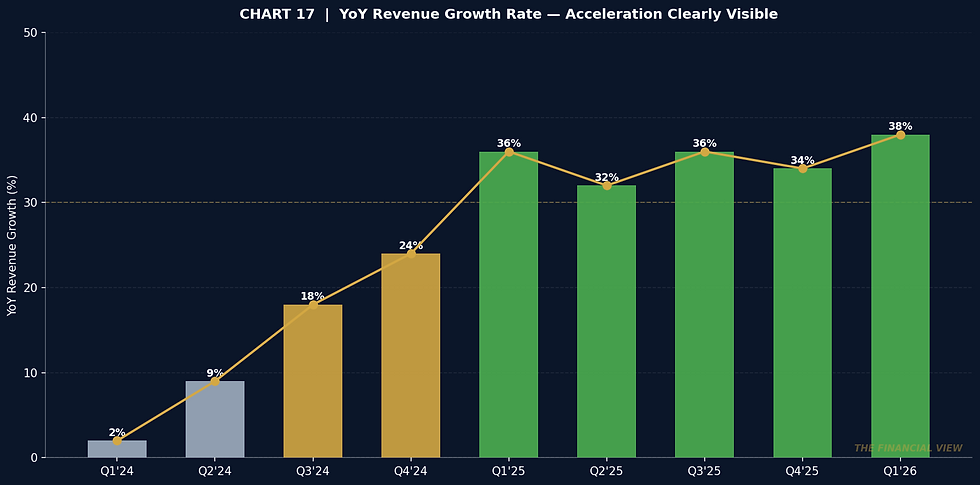

AMD enters mid-2026 as the most consequential semiconductor restructuring story of the decade. The company reported record FY2025 revenue of $34.6 billion — a 34% increase over FY2024 — and has since delivered a Q1 2026 print of $10.3 billion (up 38% year-over-year) that blew through the consensus estimate by over $400 million. Q2 2026 guidance of $11.2 billion implies 46% year-over-year growth and validates that the acceleration is not a one-quarter phenomenon.

The thesis is not simply 'AMD is growing fast.' The thesis is that AMD is undergoing a structural business model transition — from a cyclical, consumer-and-gaming-weighted chip company into a diversified AI infrastructure franchise anchored by two durable secular positions: EPYC server CPUs approaching market parity with Intel, and Instinct AI GPUs now embedded in the infrastructure roadmaps of the world's largest AI spenders. The 6-gigawatt agreements with both OpenAI and Meta — worth tens of billions of dollars in potential revenue across multiple product generations — are not marketing wins. They are architectural commitments by the two most aggressive AI infrastructure builders on the planet.

The bear case is real: NVIDIA's CUDA ecosystem is a moat that took fifteen years to build and will not be dismantled in two. AMD's ROCm software stack, while improving rapidly, still trails in developer mindshare. Export controls have already caused at least one quarter of material disruption. At a forward P/E of approximately 57x, the stock prices in meaningful execution on the MI450 and Helios ramp — a ramp not yet proven at scale.

But the bull case is structurally stronger. AMD CEO Lisa Su has revised the server CPU TAM growth forecast upward from 18% to 35% annually, projects that market to exceed $120 billion by 2030, and guided server CPU revenue growth of more than 70% year-over-year for Q2 2026. The company has $12.3 billion of cash, virtually no net debt, and generated a record $2.57 billion in free cash flow in a single quarter — 25% of revenue. The operating model is working at scale. Our base case 12-month price target is $480. Bull case: $580–640. Bear case: $220–260.

SECTION I — BUSINESS OVERVIEW & CORE THESIS

Advanced Micro Devices designs high-performance semiconductors across four operating segments: Data Center, Client and Gaming, Embedded, and Networking. Fabless — relying on TSMC for advanced node production on 5nm and 4nm processes, with next-generation Instinct GPUs expected on TSMC's 3nm CoWoS-L packaging.

One-sentence business model: AMD sells competitive compute at a lower total cost of ownership than the market leader, in markets where total cost of ownership is the primary purchase decision criterion. This is the deliberate architecture of Lisa Su's decade-long turnaround thesis — enter every market with the competitive product at a structurally lower price, then use customer relationships, cash flows, and ecosystem development to close the gap. It worked against Intel in desktop CPUs (2017). It worked in server CPUs (2% to 46.2% EPYC revenue share in seven years). The question for the next decade: can it work against NVIDIA in AI GPUs?

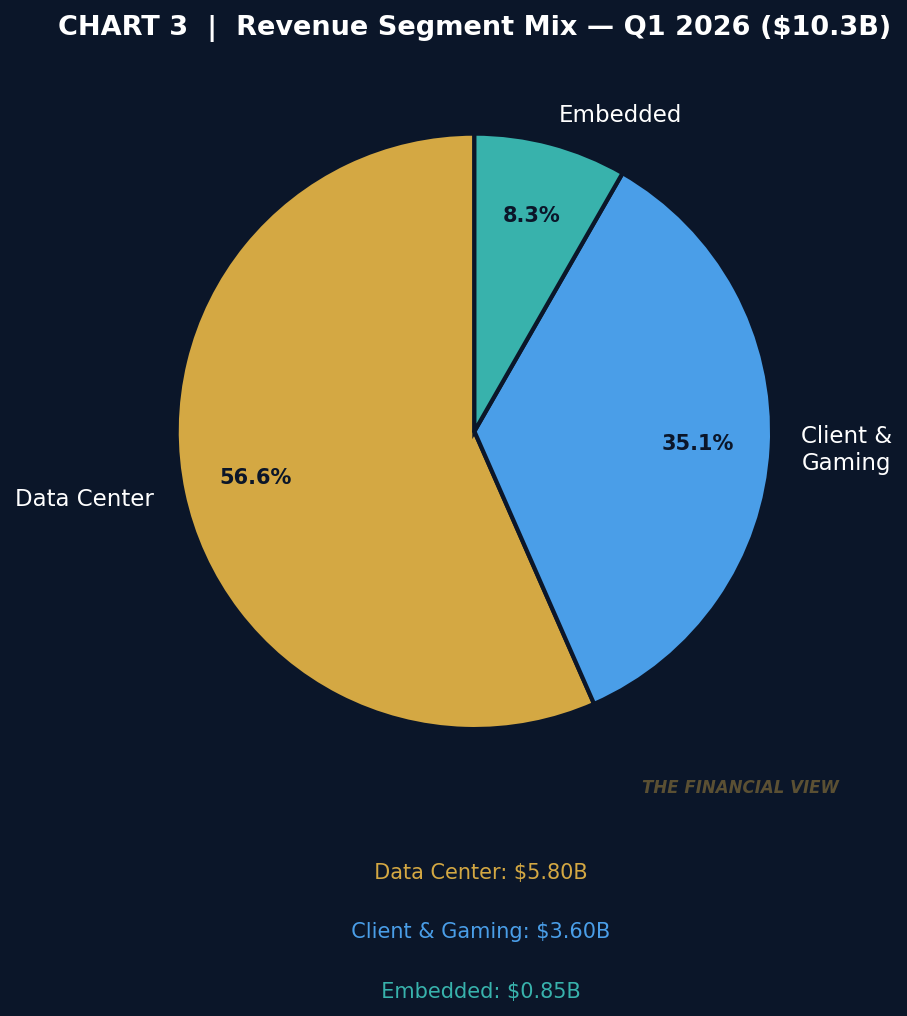

Revenue Architecture Q1 2026: Data Center $5.8B (57% of quarterly revenue), Client & Gaming $3.6B (35%), Embedded $0.85B (8%). Data Center — less than 40% of AMD's revenue just four quarters ago — has become the dominant and fastest-growing segment. AMD is transitioning from a diversified chip company into an AI infrastructure platform with a consumer hardware division attached.

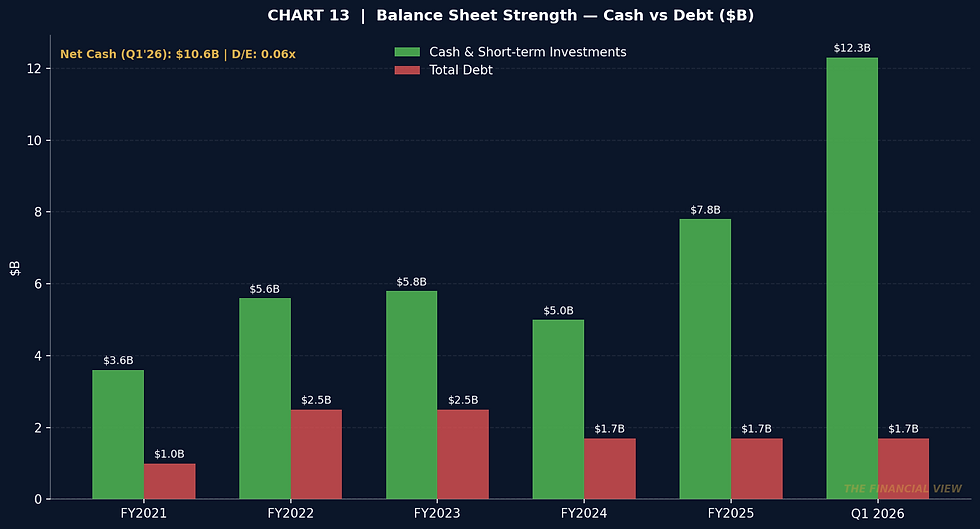

Geographic Mix: ~50% US, ~25% China (export control exposure), ~25% Europe/Japan/APAC. Balance Sheet Snapshot: $12.3B cash, $1.7B debt, $10.6B net cash, D/E 0.06x.

SECTION II — INDUSTRY & MARKET STRUCTURE

The four largest US hyperscalers collectively disclosed over $300 billion in capital expenditure budgets for 2025 alone, with AI infrastructure representing the largest and fastest-growing component. AMD's own analysis projects the server CPU TAM exceeding $120 billion annually by 2030. The AI accelerator market, estimated at $90 billion in 2025, is projected to exceed $500 billion by 2028.

The AI accelerator market is in early hyper-growth. Hyperscalers are actively seeking supply chain diversification because NVIDIA's pricing power at 70–80% gross margins creates a structural incentive to find alternatives. AMD is the only credible x86 + GPU alternative at scale. Intel's Xeon roadmap has fallen behind — aggressive discounting signals competitive desperation, not strength. AMD's EPYC Turin (5th generation) captured more than 50% of AMD's own server CPU revenue for the first time in early 2025. One structural long-term risk: ARM-based server CPUs from Amazon Graviton, Google Axion, Microsoft Cobalt, and NVIDIA's Vera chip. ARM's CEO disclosed ARM now represents approximately 50% of CPU compute share among top hyperscalers — a genuine threat, though displacement is measured in years, not quarters.

SECTION III — COMPETITIVE ADVANTAGE (MOAT ANALYSIS)

Moat Rating: Moderate — Strengthening. AMD's competitive advantage is a portfolio of partial advantages, with the key qualifier being that the moat is actively under construction rather than fully built.

Moat 1 — Lisa Su's Product Roadmap Execution (Strongest): The most underappreciated competitive advantage. When Su took over in 2014, AMD had $757M cash, a broken CPU architecture, no GPU presence in data centers, and a stock below $3. What followed: Zen CPU architecture (2017) competitive with Intel from day one. EPYC from 2% to 46.2% revenue share in seven years. Instinct from zero to 6GW commitments from OpenAI and Meta. Execution at this level compounds over time — competitors cannot replicate a management team with Su's track record by announcing roadmap plans.

Moat 2 — x86 Architecture Licensing (Durable but Eroding): AMD and Intel are the only two companies licensed to produce x86-compatible processors. The April 2026 joint x86 compatibility announcement with Intel may extend the architecture's relevance cycle against ARM pressure.

Moat 3 — EPYC Customer Switching Costs (Growing): AWS, Google Cloud, Microsoft Azure, Oracle, and Tencent all now offer EPYC-based cloud instances. Once a hyperscaler builds its software stack and procurement cycles around EPYC, migrating is expensive and time-consuming.

Moat 4 — ROCm Software Ecosystem (Weakest — But Improving): NVIDIA's CUDA platform has fifteen years of developer mindshare, millions of trained engineers, and institutional integration in every major AI framework. AMD claims day-zero compatibility with Meta Llama 4 and Google Gemma 3, but the gap in depth and breadth of the ecosystem remains real. The open-source strategy (ROCm is Apache 2.0 licensed) is smart — it enlists external developers AMD cannot afford to hire — but this is a multi-year project.

SECTION IV — MANAGEMENT & CAPITAL ALLOCATION

Lisa Su, 54, has presided over a 140-fold increase in AMD's stock price, four consecutive years of revenue records, and arguably the most successful semiconductor turnaround of the modern era. Her key strategic decisions: Xilinx acquisition ($49B, closed 2022) — controversial at the time, clearly correct in hindsight, providing FPGA IP and $3.5B in annual Embedded revenue. ZT Systems acquisition (~$5B, 2025) — added rack-scale system integration expertise critical for the Helios platform. R&D spending runs at ~$3.1B per quarter — the correct decision for a company in an arms race for AI silicon supremacy. AMD has $9.2B remaining under its share buyback authorization. No dividend — correct capital allocation for a 38%-growth company. Su owns ~$1.37B in personal AMD equity. Compensation is heavily performance-based. Red flags: None material.

SECTION V — FINANCIAL PERFORMANCE

Revenue trajectory: FY2019 $6.7B → FY2022 $23.6B (52% CAGR, pandemic/gaming era) → FY2023 $22.7B (correction: PC normalization, gaming decline, Embedded inventory cycle) → FY2024 $25.8B (+14%, uneven recovery) → FY2025 $34.6B (+34%, AI-infrastructure-led breakout) → Q1 2026 $10.3B annualized ~$41B run rate. YoY growth past five quarters: Q1 2025 +36%, Q2 2025 +32%, Q3 2025 +36%, Q4 2025 +34%, Q1 2026 +38%.

Non-GAAP gross margin: expanded from low 50s (2023) to 55% (Q1 2026), Q2 2026 guidance 56%, long-term target 55–58%. Critical context: Q2 2025 saw an $800M inventory write-down from export control restrictions on China AI chips — reported gross margin temporarily fell to 43%, creating the sharp dip visible in Chart 5. Recovered to 54% in Q3 2025. Non-GAAP operating margin: 28% in Q4 2025, 25% in Q1 2026 (elevated R&D investment ahead of MI450/Helios launch). Long-term target: 25–30%. Free cash flow: $0.75B (Q1 2025) → $2.57B (Q1 2026) — a three-fold increase in a single year, representing 25% of Q1 2026 revenue. ROIC on headline basis ~8–10%, depressed by $24B Xilinx goodwill. Tangible ROIC on core operations materially higher.

SECTION VI — BALANCE SHEET & FINANCIAL RISK

Risk Rating: LOW

Q1 2026 Balance Sheet: Cash & short-term investments $12.3B. Total debt $1.7B (long-term senior notes only). Net cash $10.6B. D/E 0.06x. Current ratio 2.72x. Inventory ~$8B — elevated, but reflects deliberate pre-positioning for MI450/Helios ramp, not obsolete stock. Operating cash flow Q1 2026: $3.0B. FCF Q1 2026: $2.57B — record. At this run rate, AMD generates ~$10B in annual FCF before reinvestment. Interest coverage is not a concern. Pension obligations minimal. No hidden liabilities of material concern. Can AMD survive a downturn? Yes, comfortably — $12.3B in cash, virtually no debt, diversified customer base.

SECTION VII — GROWTH DRIVERS & FUTURE OUTLOOK

Engine 1 — Instinct AI GPU / The 6GW Opportunity (Most Important): October 2025: AMD signs 6-gigawatt multi-year agreement with OpenAI. February 2026: Meta announces plans to deploy up to 6 gigawatts of AMD Instinct GPUs. First 1GW deployment (MI450-based) begins H2 2026. AMD CFO Jean Hu: partnership expected to deliver 'tens of billions of dollars in revenue.' Helios rack-scale architecture — AMD's answer to NVIDIA's DGX — targets Q3 2026 initial volumes, significant Q4 2026 ramp. This is the single most important product execution test of the next 12 months.

Engine 2 — EPYC Server CPU / Compounding Market Share: Server CPU TAM forecast revised from 18% to 35% annual growth, projected to exceed $120B by 2030. Lisa Su guided >70% YoY server CPU revenue growth for Q2 2026. At 46.2% revenue share, AMD is selling higher-value, higher-margin configurations than Intel on a unit basis — the definition of winning the premium market. Engine 3 — Agentic AI CPU Demand Renaissance: Agentic AI requires Lisa Su's quantification of 'at least a factor of four' more CPU compute per inference workload. If accurate, the server CPU TAM expansion story alone justifies a significant portion of AMD's current valuation. Engine 4 — Embedded Recovery: From -3% (FY2025) to 'double-digit growth' Q2 2026 guidance as inventory correction clears. $1–2B in incremental annual revenue potential.

SECTION VIII — KEY RISKS & BEAR CASE

Risk 1 — NVIDIA CUDA Lock-In (HIGH / HIGH): CUDA has 15 years of developer mindshare, integrated into every major AI framework. AMD's GPU wins at OpenAI and Meta are focused on inference, not training. Bear case: AMD's GPU business generates $8–12B annually as a profitable niche while NVIDIA captures the multi-hundred-billion training market. Risk 2 — US Export Control Expansion (HIGH / MODERATE): China is ~25% of AMD revenue. Q2 2025's $800M write-down demonstrated the damage rapid policy change inflicts. The US-China technology competition trajectory suggests this risk is permanent and potentially escalating, not a one-time event. Risk 3 — TSMC Advanced Packaging Constraints (MODERATE / HIGH): AMD's AI GPUs require TSMC's CoWoS-L packaging, which is in high demand across multiple customers. Analysts estimate AMD GPU shipments could be 15–20% below potential demand if CoWoS is constrained. AMD cannot control TSMC's internal investment allocation. Risk 4 — ROCm Maturity Gap (HIGH / MODERATE): Practical gaps in enterprise-grade support, validated software stacks, and debugging tools limit AMD's penetration below the top hyperscalers. Risk 5 — Customer Concentration: OpenAI + Meta = 12GW committed. Any financial constraint, strategic shift to internal silicon, or deployment delay at either company materially disrupts AMD's 2026–2027 ramp. Worst-Case Scenario: MI450 ramp delivers 60–70% of targeted volumes (CoWoS constraints). Export controls expand. NVIDIA GB200 proves superior enough that OpenAI pauses MI450 deployments. FY2026 revenue lands at $42–44B. Stock corrects to $250–280. Not the base case — but every serious investor must explicitly price this before initiating a position.

SECTION IX — VALUATION ANALYSIS

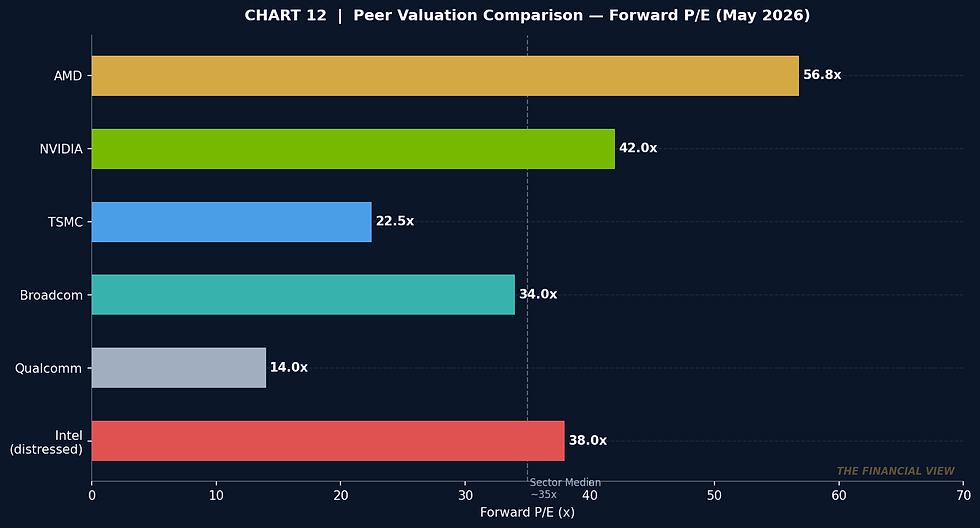

Current Valuation (May 20, 2026): Market Cap $686B. EV ~$678B. Trailing P/E (GAAP) ~140x — inflated by Xilinx amortization, not economically meaningful. Forward P/E (non-GAAP) ~48–57x. EV/EBITDA ~84–91x. FCF yield ~1.5% trailing, rising to 3–4% on FY2026 estimates. PEG ratio ~0.84–1.01 — the most important number for a high-growth company. Peer Comparison: NVIDIA ~42x forward P/E (but 75% GAAP gross margins vs AMD's 53%). TSMC ~22x. Broadcom ~34x. Qualcomm ~14x. Peer median ~35x. AMD's 56x forward P/E carries a 60% premium — justifiable only if AMD sustains 30%+ revenue growth through FY2027. DCF — Base Case (27% CAGR, 24% terminal FCF margin, 10% discount rate): Intrinsic value $420–480. Bull case (32% CAGR, 28% FCF margin): $580–640. Bear case (18% CAGR, 18% FCF margin): $220–260. Verdict: Fairly valued with slight richness at $416. Attractive in the bull scenario. Entry at $380–395 offers materially better risk-reward.

SECTION X — MARKET EXPECTATIONS vs REALITY

The AMD bull case has moved from niche view to consensus. 49 covering analysts had an average target of $307–358 before Q1 2026 — AMD has already blown through that. The entire sell-side coverage universe is in catch-up revision mode: bullish in the near term (revision momentum), but the easy narrative re-rating money may be behind us. What the market gets wrong: benchmarking AMD's GPU business against NVIDIA's training-centric model. AMD is positioning as the inference-first, cost-efficient alternative for deployed production AI. The inference market, as AI moves from development to deployment at scale, could be structurally larger than training over a multi-year period. The market also isn't fully pricing the agentic AI CPU demand expansion — Lisa Su's 4x CPU compute per inference workload figure implies a server CPU TAM expansion that alone justifies significant AMD valuation without requiring flawless GPU execution. Key catalyst to watch: H2 2026 MI450/Helios shipment volumes. Confirmation in the Q2 2026 earnings call (August 2026) that Helios is ramping as planned → clear path to $480–520. Any slippage → multiple compresses fast.

SECTION XI — FINAL INVESTMENT VERDICT

AMD is a fundamentally different company than it was five years ago. 46.2% x86 server CPU revenue share approaching parity with Intel. Only credible x86 + GPU alternative to NVIDIA in AI data center infrastructure. 6-gigawatt committed partnerships with both OpenAI and Meta. $12.3B cash, $1.7B debt. One of the best CEO execution track records in technology. Q1 2026: $10.3B revenue (+38%), $2.57B FCF (record), $11.2B Q2 2026 guidance (+46%). The operating model is showing leverage — non-GAAP EPS grew 43% while revenue grew 38%.

Investment Call: STRONG BUY | 12-month price target: $480 (base case) Risk-reward at $416 is favorable for investors with a 12-month+ time horizon who accept material execution risk. The stock is fairly valued, not a deep value bargain — the thesis is predicated on continued execution, not multiple expansion from a depressed base. For new positions, scaling in on pullbacks toward $380–395 improves risk-reward materially. Bull case $580–640 by end of 2027 if MI450/Helios executes and the OpenAI/Meta gigawatt deployments proceed. Bear case $220–260 requires both execution disappointment and macro/regulatory headwinds simultaneously. Rating: ⭐⭐⭐⭐½ — Strong Business, Executing at Scale, Slight Valuation Premium to Base Case

The Financial View | Research Division | May 2026 | "Institutional thinking. Independent perspective."