ABB: Built for the Next Watt

- The Financial View

- Apr 24

- 18 min read

A Swiss industrial at the center of electrification, automation, and AI power.

The Financial View · Equity Research · Issue 07 · April 2026

Ticker: SIX:ABBN · Price (Apr 20): CHF 74 · 12-month target: CHF 86 · Rating: BUY

1. The one-page call

I am buying ABB into the Q1 2026 print on April 22. Not because the quarter itself will be a blowout (it probably won't), but because the setup for the next four quarters is the cleanest this stock has offered in a decade. You have a CEO who inherited Björn Rosengren's decentralized operating system and is running it with less theater and more compounding. You have a Robotics business that is about to walk off the balance sheet at $5.375bn enterprise value, which unlocks roughly $5.3bn of net cash and removes the single lowest-return drag on group ROCE. You have an Electrification business that owns the short-cycle power-kit layer the AI data-center buildout runs on, growing mid-teens organically with margins that have quietly walked from 17% to 23% in four years. And you have a Swiss industrial conglomerate trading at 22x forward EBITA, which sounds expensive until you price the pieces separately.

My base case is CHF 86 per share on a sum-of-the-parts, 16% upside from the April 20 close. Probability-weighted against a bull case of CHF 99 and a bear case of CHF 64, the expected value is CHF 84. That is a real 13% return on a stock most large-cap industrial books still carry at neutral.

What follows is the full work behind that call. What I stress-tested, what I think the market is under-pricing, and what would make me change my mind.

2. Why now, and why this way

Every equity research note should start by answering one question: what does the market have wrong, and why do I think so. Here is my answer.

The market is pricing ABB as a cyclical European industrial with a good operating story and a decent dividend. That is not wrong. It is just incomplete. Three things are converging that the forward multiple does not yet fully reflect.

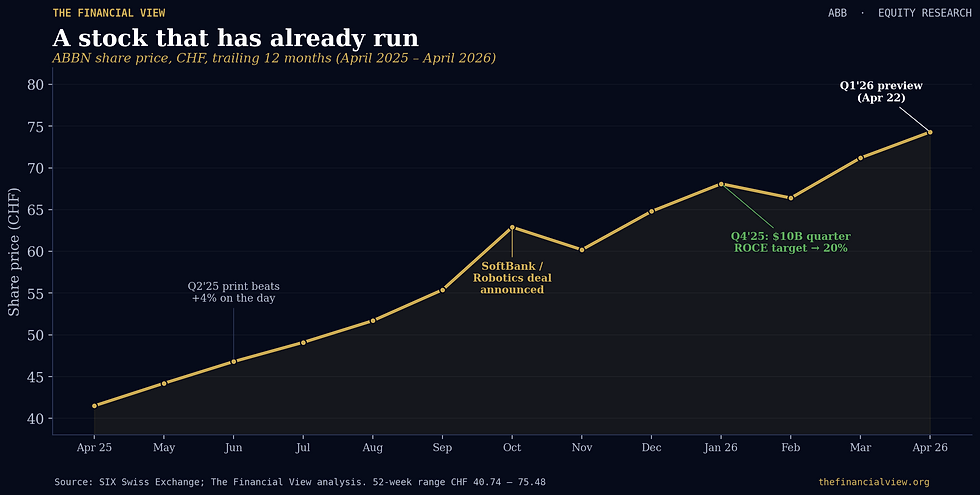

First, Robotics is leaving the house. The SoftBank deal was announced on October 8, 2025 at $5.375bn enterprise value. ABB expects around $5.3bn of net cash proceeds and a $2.4bn pre-tax book gain at close. Close is guided to mid-to-late 2026. Robotics has been the lowest-margin, highest-capex, most cyclical business inside ABB for years. Removing it raises group operating margin by roughly 80 basis points on a mix basis alone, and the cash hits the balance sheet right when management is running one of the more disciplined capital-return programs in European industrials.

Second, Electrification is not just growing. It is growing at the part of the S-curve where AI data-center power demand collides with grid reinvestment. Roughly 9% of group revenue today is data-center exposed. That slice is growing high-teens organically, with embedded NVIDIA partnership work on medium-voltage AC to the rack. This is not a theme. This is order book.

Third, Morten Wierod is, in my read, doing something Björn Rosengren started but could not finish. Rosengren took a bureaucratic Swiss-Swedish matrix and broke it into roughly twenty autonomous divisions with their own P&L accountability. Wierod is running that same operating model without the restructuring noise, and the margin compounding is showing up cleanly. He has announced the collapse of the four business areas to three in Q1 2026 (Machine Automation moves from Robotics & Discrete Automation into Process Automation, which then rebrands simply to Automation). The signal inside that is bigger than the org-chart change.

None of this is priced as an integrated thesis. Each piece shows up in segment commentary. No analyst I have read stitches it together.

3. What ABB actually is

ABB Ltd is a Swiss-Swedish industrial technology company headquartered in Zürich. Primary listing is on SIX (ABBN). Market cap at the April 20 close is roughly CHF 128bn. FY25 revenue was $33.22bn. FY25 operational EBITA margin was 19.0%. Group ROCE was 23.4%.

Said simply, ABB does four things. It electrifies buildings, factories, and infrastructure (Electrification). It builds the motors, drives, and traction systems that move physical stuff (Motion). It builds the control systems and instrumentation that run continuous-process plants like oil refineries, chemical lines, and paper mills (Process Automation). And until it closes the SoftBank deal, it builds industrial robots and discrete-motion control systems (Robotics & Discrete Automation).

From Q1 2026 forward, the structure compresses. Machine Automation, the B&R Austria piece that used to sit inside RDA, moves into Process Automation. The renamed Automation business area is then the combined continuous-process and discrete-machine control layer. Robotics continues to report as a standalone segment through close. Four areas become three.

The underlying divisions are where the real story lives. Electrification has five: Smart Buildings, Smart Power, Distribution Solutions, Installation Products, and Smart Infrastructure / E-mobility. Motion has six: Large Motors & Generators, IEC Low Voltage Motors, NEMA Motors, System Drives, Drive Products, Traction. And the newly formed Automation houses Process Industries, Energy Industries, Measurement & Analytics, Marine & Ports, Process Control Platform, Machine Automation (B&R), and Discrete Automation.

Each division has its own general manager, its own P&L, and its own capital allocation discipline. That is the Rosengren system. Wierod has not touched it.

4. From Rosengren to Wierod: continuity with a different temperature

Björn Rosengren ran ABB from March 2020 to August 2024. He inherited a company that had spent the 2010s in restructuring mode and a matrix that had fossilized. He broke it into divisions. He pushed through the Power Grids divestment to Hitachi. He cleaned out the portfolio. He set the ABB Way: decentralized operating model, strict accountability, no HQ meddling.

Morten Wierod took over in August 2024. He is a twenty-year ABB veteran, most recently the president of the Electrification business area. He is Norwegian, quiet, and operationally oriented. He does not do the tent-revival tone Rosengren sometimes used on earnings calls.

Here is why that matters. Rosengren's operating model was the right system. It worked. But it was also his story, and CEO transitions in conglomerates often come with a "new era" pitch that breaks the very thing that was working. Wierod has resisted that. He has not announced a new strategic framework. He has not reorganized the divisions. He has not added headcount at group. He has continued buybacks, continued the dividend, and continued the bolt-on M&A pattern Rosengren started. The Q1 2026 collapse of four areas to three is the only structural move he has made, and it is consistent with Rosengren's simplification logic rather than a reversal of it.

I read this as a positive. The market sometimes punishes continuity-CEOs because there is no new narrative to sell. In industrials, continuity is often the alpha. Wierod is running a proven operating system without the restructuring cost line, and the numbers are showing through.

5. The SoftBank Robotics deal, in detail

On October 8, 2025, ABB announced the agreement to sell its Robotics division to SoftBank Group at an enterprise value of $5.375bn. Terms disclosed: approximately $5.3bn in net cash proceeds to ABB, a $2.4bn pre-tax book gain expected at close, close guided to mid-to-late 2026 pending regulatory approvals across the US, EU, and China.

Robotics in FY25 did roughly $2.3bn of revenue with operating EBITA margin in the low-double-digits. Inside ABB it has been structurally the lowest-return business area. Capital intensity is higher than Motion or Electrification. Margin volatility is higher. The end market is meaningfully more cyclical, particularly the automotive exposure.

The math on removing it is clean. Group FY25 operational EBITA margin was 19.0%. Excluding Robotics at its FY25 contribution, pro forma group margin lifts roughly 70 to 90 basis points. Group ROCE, which was 23.4% FY25, rises materially because the capital base falls faster than earnings. My estimate: pro forma group ROCE approaches 28% post-close on a mix basis.

On the cash side, $5.3bn net cash at close is large relative to ABB's current net debt of approximately $4bn. Post-close, ABB will be in a small net-cash position for the first time since the Power Grids sale. I expect management to announce an incremental buyback at that point. The Rosengren-era framework was to return excess cash above a 1.5x net-debt-to-EBITDA target through buybacks and dividends, and Wierod has not signaled any change to that.

The risk here is not the deal itself. The risk is the regulatory path. SoftBank is a Japanese buyer acquiring a global robotics franchise with meaningful China and US exposure. I assign roughly 15% probability to the deal being blocked or renegotiated down. In that case, ABB would revert to the pre-announcement structure and the stock would likely give back most of the post-October run-up. That is a meaningful downside scenario I account for in the bear case.

6. The data-center thesis, sized properly

Data centers are where I think the market is most underestimating ABB today. The gross-up is simple. AI training infrastructure requires medium-voltage power distribution at scale. Rack density is climbing from ~30 kW per rack toward 100+ kW. That change requires a different electrical topology, closer to what industrial facilities have used for decades. ABB sells exactly that kit.

Today, data-center-exposed revenue is approximately 9% of group, or roughly $3bn annualized. The relevant slice sits mostly inside Electrification's Smart Power and Distribution Solutions divisions. Growth in that sub-segment has been running north of 20% in the last four quarters. ABB is currently in a public development partnership with NVIDIA on medium-voltage AC distribution directly to the rack, announced in mid-2024 and expanded in 2025.

Here is the more important point. The unit economics of data-center power kit are better than group average Electrification margins. I model data-center mix at roughly 27% operating EBITA margin versus Electrification group margin of 23%. As the mix share climbs from 9% of group toward 12 to 15% over the next three years, the embedded mix shift alone is worth roughly 40 to 60 basis points of consolidated operating margin.

The objection is that this is a cyclical spend category and the hyperscaler capex cycle will roll over. Maybe. But ABB sells a pick-and-shovel layer that cuts across all the hyperscalers and most of the colocation builders. It is not exposed to one customer's capex decision. And the installed base for this generation of power kit has to be refreshed in ways the previous generation did not. I am not pricing this as a permanent growth rate. I am pricing it as a three-year mix shift with meaningful margin lift.

7. Electrification: the crown jewel, and why it is not fully priced

Electrification is 47% of group revenue and the highest-margin business area at roughly 23% operating EBITA. Organic growth has been running in the high-single-digits to low-teens for eight straight quarters. The order book is at record levels. Book-to-bill has been above 1.0 for ten consecutive quarters.

Inside the five divisions, two matter most for the forward story. Smart Power, which houses the data-center power-kit business and the UPS franchise, is the fastest-growing piece of the entire company. Distribution Solutions, which sells medium-voltage switchgear into utilities and industrial customers, is the most exposed to the global grid-reinvestment cycle that is now running through US, Europe, and Middle East utility capex budgets.

On peer comps, the closest analog for Electrification is Schneider Electric and Eaton. Schneider trades at around 26x forward EBITA. Eaton trades at 28x. ABB's Electrification business on a standalone multiple should be at or slightly above Schneider given mix and margin trajectory. In the SOTP I use 24x, which is conservative. Each turn of multiple on Electrification is worth roughly CHF 5 per ABB share.

8. Motion: the quiet compounder

Motion is 23% of group revenue at approximately 18.5% operating EBITA margin. It is not the glamour segment. It is the foundation. If you run a factory, a railway system, a building, or a ship, Motion sells you the motor-plus-drive combination that moves the thing.

The forward story here is structural and simple. Regulatory efficiency standards on electric motors are tightening globally. IEC and NEMA standards are pushing industrial motor efficiency classes upward, which forces installed-base replacement. System Drives has a particular tailwind from renewable-integration work: wind turbine drives, battery storage inverters, industrial-scale heat pumps. Traction has a long-cycle tailwind from passenger rail modernization across Europe and Asia.

Motion grows mid-single-digits organically with margin expansion of 20 to 40 basis points per year on a mix basis. That is not exciting on a quarterly basis. It compounds beautifully over five years. At 17x forward EBITA in the SOTP, Motion is worth roughly CHF 21 per ABB share.

9. Process Automation (soon: Automation): the underappreciated reflation trade

Process Automation is 21% of group revenue at approximately 16% operating EBITA margin. From Q1 2026, the business absorbs Machine Automation (B&R Austria) and rebrands to Automation, bringing the business area closer to 30% of group revenue at mid-to-high-teens margins.

This is the most interesting operating turnaround story inside ABB right now and the one I think sell-side is least focused on. The business has lagged on margin for four years. It has under-earned relative to Emerson Process, which runs at mid-to-high-20s operating margins on a comparable mix. The gap has been roughly 800 to 1000 basis points.

The closure of that gap is what the Machine Automation transfer enables. Combining the continuous-process control stack (the legacy ABB piece) with the discrete-machine control stack (B&R) into one business area creates a wider software and services attach point. Services and software mix lift margin. The trajectory I model is Automation operating margin moving from 16% FY25 toward 19% by FY28, which is worth roughly CHF 7 per share on its own.

This is a show-me story until the first post-integration quarterly print, which will be Q1 2026 on April 22. I am watching the segment commentary on this one more carefully than any other line item.

10. Robotics & Discrete Automation: held for sale, managed for continuity

For modeling purposes, Robotics is on the balance sheet through close. FY25 revenue was roughly $2.3bn, roughly 7% of group, with margin in the low-double-digits. Until close, ABB will continue to operate it, book its revenue and earnings, and report it as a held-for-sale segment under IFRS 5.

The operational question here is whether the business degrades during the hold period. SoftBank has signaled continuity of management and limited pre-close integration work. ABB has signaled the same. My baseline assumption is that Robotics contributes roughly as it did in FY25 through the transaction close, with a modest working-capital unwind in the final quarter before close. The $2.4bn pre-tax book gain is locked at the announced transaction value and crystalizes at close.

Post-close, Robotics is a non-event for ABB modeling. Before close, I value it inside the SOTP at the disclosed $5.375bn enterprise value, net of estimated tax and transaction costs, which nets to approximately $5.3bn of cash.

11. The FY25 print, in one paragraph

Group revenue FY25 was $33.22bn, up 6% reported and 7% organic. Operational EBITA was $6.31bn, margin 19.0% vs 18.1% prior year, a 90 basis point expansion. Net income was $4.04bn. Free cash flow was $4.41bn, a 103% conversion on net income. Order book climbed to record levels, with book-to-bill averaging 1.05 across the year. Electrification grew organic revenue +12%, Motion +6%, Process Automation +4%, Robotics & Discrete Automation +3%. Operating EBITA margin by area: Electrification 23.0%, Motion 18.6%, Process Automation 16.1%, RDA 11.2%.

If you only read one number, it is the 90 basis point margin expansion in a year where group organic growth was 7%. That is operating leverage showing through the decentralized model. It is not mix. It is execution.

12. Book-to-bill, orders, backlog

ABB reports book-to-bill quarterly. It has now been above 1.0 for ten straight quarters. Order backlog at year-end FY25 was approximately $22bn, which is roughly 66% of FY25 revenue and a record.

The composition of the backlog matters as much as the size. Roughly 55% is Electrification, biased toward utilities, data centers, and infrastructure. Roughly 25% is Motion, biased toward long-cycle industrial and rail. Roughly 20% is Process Automation / Automation, biased toward energy and chemicals. The average duration of the backlog has lengthened from about 7 months four years ago to about 10 months today, reflecting the shift toward larger systems projects with longer revenue-recognition tails.

A rising, lengthening backlog at above-trend organic growth is the strongest forward-revenue signal an industrial can print. Book-to-bill below 1.0 for even one quarter would be a warning. I will be watching Q1 2026 for exactly that.

13. Free cash flow, capital allocation, balance sheet

FY25 free cash flow was $4.41bn, which represents 103% conversion on net income and roughly 13.3% of revenue. Capex has held at approximately 2.1% of revenue, below industrial peer medians. Working capital has been a modest source of cash as the order mix has tilted toward longer-dated contracts with better milestone billing terms.

Capital allocation priority stack, per management guidance and observed behavior: dividend (raised annually, payout ratio around 50%), organic growth capex (~2% of revenue), bolt-on M&A (disciplined, roughly $500m to $1bn per year in aggregate), share buybacks (an active $1bn program through FY26).

Net debt at FY25 year-end was approximately $4bn, or 0.63x EBITDA. Post SoftBank close, ABB will be in net cash. I expect management to raise the buyback envelope by approximately $2bn over the subsequent two years. I do not expect a large transformational M&A move. That is not the Wierod playbook.

14. The SOTP valuation, worked

Sum-of-the-parts is the right framework for ABB because the business areas have distinct end markets, margin profiles, and peer comps. Blending them into a single group multiple understates the quality mix.

Here is the build.

Electrification: FY26E EBITA of $3.68bn at 22x. Peers Schneider at 26x, Eaton at 28x. I discount to 22x for ABB's slightly lower data-center mix share today. Equity value contribution: $81bn.

Motion: FY26E EBITA of $1.50bn at 17x. Peer Siemens drives business implied at ~16x, Rockwell at ~20x. Blended 17x is mid-range. Equity value contribution: $25.4bn.

Automation (combined PA + Machine Automation): FY26E EBITA of $1.09bn at 14.75x. Emerson Process at 20x, Honeywell PMT at 18x. I discount to 14.75x because the margin convergence is not yet visible in the print. Equity value contribution: $16.1bn.

Robotics (held for sale): disclosed enterprise value $5.375bn at close, net of transaction costs. Contribution: $5.3bn cash equivalent post-close.

Corporate and unallocated costs: -$3.2bn.

Net debt and pension: -$4.0bn.

Implied equity value: $127.9bn, or roughly $128bn.

At 1.84bn diluted shares and 1.24 USD/CHF, the per-share target is CHF 86.

The blended implied multiple on group FY26 EBITA is 21.7x, which is roughly in line with where ABB trades today at 22x. In other words, the market is paying the right multiple for the blend but not giving ABB credit for the premium-peer multiple Electrification should command on its own. Close that gap and the stock reprices.

15. Peer comparison

ABB at 22x forward EBITA sits in the middle of the European-US industrial-tech peer set. Schneider Electric 26x. Eaton 28x. Siemens 18x. Rockwell Automation 20x. Honeywell 18x. Emerson 20x.

The correct comparison is not ABB vs the group median. The correct comparison is ABB's Electrification business vs Schneider and Eaton, because that is where the marginal investor is deciding between three picks. On that basis, ABB is cheaper than Schneider by four turns and cheaper than Eaton by six turns, with comparable growth, comparable margin trajectory, and a pending portfolio unlock (Robotics) that Schneider and Eaton do not have. That is the arbitrage.

16. Capital returns: the quiet cash return story

ABB paid a CHF 0.90 dividend on FY24 earnings, yielding roughly 1.2% on spot. The FY25 dividend, to be paid in Q2 2026, has been indicated by management at CHF 0.98 to CHF 1.00, implying roughly 9 to 11% dividend growth. At current price, that is a yield of 1.35% forward.

The more important return vehicle is the buyback. ABB has a $1bn program active through end-FY26 and has completed roughly $3.5bn in cumulative buybacks over the last three years, shrinking the diluted share count by roughly 2% per year. Post SoftBank close, I expect that rate to step up. The cumulative effect of 2 to 3% annual share-count reduction compounding against high-single-digit top-line growth is more powerful than the dividend line.

17. Q1 2026 earnings preview: what I am watching, what I think prints

ABB reports Q1 2026 on April 22, 2026, pre-market European time. Consensus is looking for approximately $7.8bn in revenue (organic +5%) and operational EBITA margin of 19.4%.

Here is my read on the specific lines.

Revenue: I think the top-line will be in line to slightly above consensus. Electrification should deliver +11% organic. Motion should deliver +5%. The newly combined Automation line will be the noisy piece: the accounting transfer of Machine Automation from RDA to PA happens in this quarter, which will make prior-year comparisons messy. Management will have to walk through the restated segment panel carefully. I would not be surprised if the headline Automation organic number looks soft on the print and management spends time on the call explaining the reclassification.

Margin: I expect a beat of 10 to 20 basis points on operational EBITA margin vs consensus. The main driver is mix (Electrification up-weighting) and ongoing cost discipline. Robotics margin is likely to be softer sequentially given the held-for-sale status. That should not affect the read-through.

Orders: this is the most important line for the forward story. I want to see book-to-bill at or above 1.05, which would extend the streak to eleven straight quarters. Anything below 1.0 is a yellow flag. Order momentum in Electrification specifically is what the stock will trade on.

Guidance: I do not expect a guidance raise on the Q1 print. Wierod is not a guide-up-early CEO. The most likely commentary is reaffirmation of the prior framework of mid-single-digit organic growth and operating margin in the upper half of the 16 to 19% long-term range.

SoftBank update: management will give a process update on the Robotics sale. I am looking for confirmation that regulatory filings are tracking to schedule and no changes to the mid-to-late 2026 close timing.

The print itself is probably a modest beat and a grey-flag-to-green day. The real trade is the setup for the next three quarters, not the single print.

18. The bull case: CHF 99

What has to happen for the stock to be at CHF 99 in twelve months. Electrification organic growth accelerates from low-teens to mid-teens as data-center power kit orders step up. Group margin walks to 20% or better by year-end. SoftBank deal closes on the early end of the guided window, freeing up the cash return step-up by Q4 2026 rather than FY27. Automation business integration shows clear margin convergence toward Emerson on the first two post-integration prints. Multiple re-rates to 24x on a higher-quality earnings mix.

Probability: 25%.

19. The base case: CHF 86

What has to happen for the stock to be at CHF 86 in twelve months. Group revenue grows 6 to 7% organic, in line with FY25 trajectory. Margin expands another 40 to 60 basis points, a deceleration from FY25's 90 bps but consistent with mix trajectory. SoftBank closes mid-2026 as guided. Buyback pace steps up modestly. Automation margin convergence is visible but not dramatic. Multiple holds at 22x forward EBITA.

Probability: 55%.

20. The bear case: CHF 64

What has to happen for the stock to be at CHF 64 in twelve months. European industrial capex rolls over as eurozone growth softens. US tariff environment worsens and pressures Electrification's US pricing. Data-center order momentum slows, not collapses. SoftBank deal hits regulatory delay, pushes close into FY27 or gets renegotiated down in price. Group margin flat to modestly down as mix tailwind is offset by volume deleverage. Multiple compresses to 18x.

Probability: 20%.

Probability-weighted target: 0.25 × 99 + 0.55 × 86 + 0.20 × 64 = CHF 84.30. Base case target of CHF 86 is the published target, with the probability-weighted figure as a sanity check.

21. What would change my mind

Three things would force me off this call.

First, a clean break in Electrification orders. If book-to-bill drops below 1.0 on the Q1 print and management commentary pivots from "strong order momentum" to "stabilizing at lower levels," the data-center and grid-reinvestment thesis is wrong on timing, and the forward multiple compresses.

Second, SoftBank deal collapse or material renegotiation. The $5.3bn of net cash is inside my SOTP and inside my expectation for the cash-return step-up. Losing it does not invalidate the operating story, but it takes CHF 5 to 7 of per-share value off the table and erases the clean portfolio-simplification narrative.

Third, a Wierod capital-allocation surprise. If management announces a large transformational acquisition that leverages the balance sheet above 1.5x net-debt-to-EBITDA, the continuity thesis is broken. I am not expecting this. I am watching for it.

22. Risks I am explicitly accepting

FX. ABB reports in USD but has meaningful EUR and CHF cost bases and a broad revenue footprint. A sharp USD move in either direction materially affects reported EBITA. I am assuming a roughly stable USD at 1.24 USD/CHF in the SOTP.

Cyclical end markets. Robotics is the most cyclical piece, and it is leaving. Motion has residual cyclicality through industrial automation capex. Electrification's utility exposure partially offsets this, but the data-center mix is newer and could prove more cyclical than hyperscaler commitments currently suggest.

China. ABB has a meaningful China installed base and revenue exposure, particularly in Motion and Robotics. Geopolitical deterioration or a China industrial downturn would pressure both the ongoing operation and the SoftBank regulatory path.

Execution on Automation integration. The Machine Automation transfer into PA is a live integration risk. If the first two post-merger prints show revenue dis-synergies or margin slippage rather than convergence toward Emerson, the Automation re-rating leg of the thesis is delayed.

23. What this is not

This is not a macro trade. I am not pitching ABB because I think European industrial capex is going to inflect higher globally in 2026. I do not have a strong view on that. The setup works even if eurozone industrial activity is flat and US growth cools modestly from current trajectory, because the thesis is driven by company-specific portfolio actions, company-specific margin mechanics, and company-specific multiple arbitrage.

This is also not a momentum trade. ABB has already run. The stock is up roughly 18% in the twelve months to April 20, 2026. If you are looking for a deep-value entry point, this is not it. What you are buying here is a high-quality compounder at a reasonable multiple with a clean portfolio catalyst.

24. How I am sizing this

For a diversified book, I carry ABB at a 4 to 5% position size. That reflects my confidence in the base case but accounts for the two material downside risks (SoftBank regulatory path, eurozone industrial capex rollover) that could drive the bear case. I add to a 6% position on a clean Q1 print where book-to-bill prints above 1.05 and the Automation segment commentary confirms the integration is on track. I trim back toward 3% if book-to-bill breaks below 1.0 or management signals SoftBank delay.

Entry: any price below CHF 78 is clean. Between CHF 78 and CHF 84, you are paying for most of the probability-weighted upside upfront. Above CHF 86, the risk-reward flips unfavorable.

25. The bottom line

ABB is a Swiss industrial conglomerate running a proven decentralized operating system under a continuity CEO who is letting the machine compound without getting in its way. It is selling its lowest-return business at a full price and will be in a net-cash position within twelve months. Its largest segment owns the kit layer the AI-power buildout runs on, growing mid-teens with 23% operating margins. Its newly combined Automation business is an underappreciated margin-convergence story. The multiple is mid-pack on the group but does not give credit for the premium-peer comp on Electrification.

My target is CHF 86, implying 16% upside from the April 20 close of CHF 74. Probability-weighted target is CHF 84. Rating: BUY.

The Q1 print on April 22 is a setup quarter, not a catalyst quarter. The real catalyst sequence is Q2 (first post-Machine-Automation integration print), H2 2026 (SoftBank close and cash deployment), and FY26 full-year (first full year of the three-business-area structure at scale).

I am long into the print. I expect to be long through the cycle.

The Financial View. Equity research for founders, operators, and serious capital allocators. thefinancialview.org

Analyst: Vansh Agarwal. Published: April 21, 2026. This report reflects the author's independent analysis and does not constitute investment advice. The author may hold positions in securities mentioned.